After a storm or sudden roof issue, many Florida homeowners wonder: “Will my insurance cover this roof repair?” The answer depends on several factors especially here in the Sunshine State, where hurricanes, windstorms, and tropical weather are common.

At SPC Roofers, we’ve helped Northeast Florida homeowners navigate roofing claims for decades. Here’s what you need to know to determine if your roof repair may be covered by your insurance provider.

Determine the Cause of Damage

Insurance typically covers sudden, accidental damage such as a recent storm blew off shingles or caused a leak, you may have a strong case for coverage.

Covered events often include:

-

Wind or hurricane damage

-

Hail impact

-

Falling trees or debris

-

Fire or lightning

-

Vandalism

Not typically covered:

-

General aging or deterioration

-

Improper installation or poor maintenance

-

Damage from prior unresolved issues (like long standing leaks)

Check Your Insurance Policy

Look for your dwelling coverage and specific wording about your roof. Florida policies vary by company, but here are some key details to review. Wind/Hurricane deductible: Often a percentage of your home’s insured value, not a flat fee. Roof depreciation or age limit: Older roofs typically over 10–15 years may have limited coverage. Actual Cash Value vs. Replacement

Cost Value : Actual cash value policies only pay for the roof’s depreciated value. Replacement cost value policies may cover full replacement, minus your deductible.

Get a Professional Roof Inspection

Before you file a claim, get a photo documented inspection from a licensed Florida roofing contractor like SPC Roofers. Filing unnecessary claims can raise premiums or get you dropped so it’s smart to get expert input first. At SPC roofers we inspect the full roof system such as the shingles, flashing, vent and underlayment. Identify storm related vs. wear related issues. Provide a detailed damage report and help you decide if a claim is worth filing.

File a Claim Promptly if Damage Is Valid

In Florida, you generally have one year from the date of loss to file a roof claim. If we identify storm related damage you’ll file the claim with your insurance company, they’ll assign an adjuster to inspect the roof and we can meet the adjuster onsite to ensure they see everything.

SPC Roofers helps walk you through the process and ensures you’re not navigating it alone.

Check out this recent review for SPC Roofers:

“I just wanted to thank SPC and my rep Rick Taylor. It was my first time replacing my roof and they were there every single step of the way. I love the finished product and would recommend SPC to anybody!”

Understand What the Adjuster Approves

After your insurance adjuster completes their review, they’ll issue a claim summary, outline what’s covered, minus your deductible and determine whether a full roof replacement or partial repair is warranted. We’ll review their summary with you and explain next steps. If anything is missed, we can help request a supplement or reevaluation.

Real Job Highlight: Roof Repair Covered in Jacksonville

One of our Jacksonville customers had roof leaks after a sudden summer windstorm. They weren’t sure whether it would be covered, but SPC Roofers documented missing shingles, uplifted flashing, and water damage all caused by wind. We helped them file the claim, met the adjuster, and their roof repair was fully covered except for their deductible. The repair was completed within days with Owens Corning materials and a written warranty.

Peace of Mind With a Trusted Local Roofer

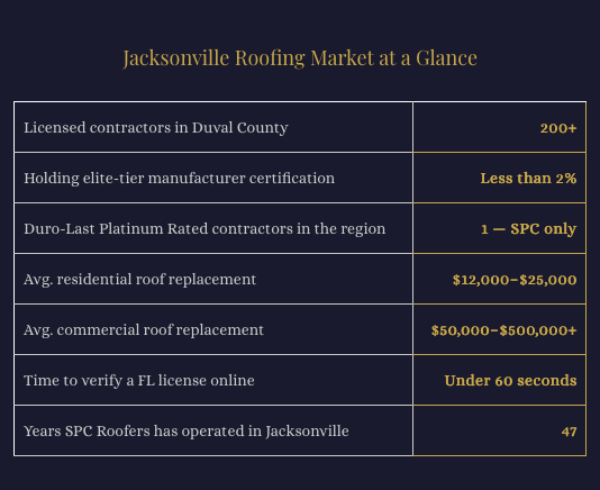

If you’re unsure whether your roof damage qualifies for coverage, don’t guess. SPC Roofers has served Jacksonville and Northeast Florida homeowners since 1978. We’re licensed, insured, and experienced in helping Florida families protect their homes and navigate insurance claims with confidence.